The valuation effects of index investment in commodity futures (with M. Dubois)

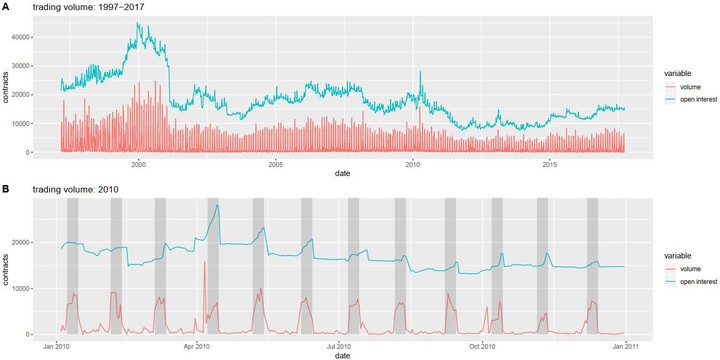

Monthly trading volume spikes in GSCI futures

Monthly trading volume spikes in GSCI futures

This paper studies the valuation effect of the SP-GSCI roll on commodity contracts. We identify a surge of investment tracking commodity futures indices in December 2003. Before 2004, the roll period generated average cumulative abnormal price changes amounting to 115 bps for the nearby contract and 146 bps for the first deferred contract. From 2004 to 2010, the average cumulative abnormal price changes of the nearby (first deferred) is equal to -60 bps (-40 bps). However, a strategy that front-runs the roll does not generate abnormal profits at the contract level after (reasonable) transaction costs. A difference-in-differences regression confirms that the financialization has an alleviating effect, with the nearby (first deferred) average cumulative abnormal price changes showing a 158 (166) bps drop, statistically significant at the 1% level. The introduction of electronic trading alone has no effect on abnormal price changes during the roll. Finally, the contemporaneous change in hedging pressure is negatively related (statistically significant at the 1% level) to cumulative abnormal price changes, while the contemporaneous change in the commodity index pressure, average hedging pressure, and cross (average) hedging pressure does not affect cumulative abnormal price changes.