A tale of two premiums revisited

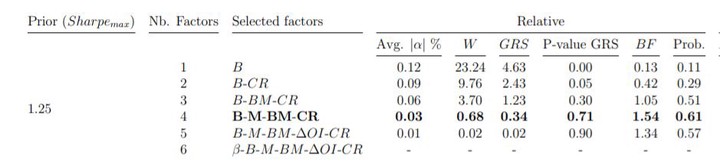

Bayesian optimal factor selection

Bayesian optimal factor selection

This paper investigates the effect of the “financialization” of commodity markets in terms of pricing. I explore whether the emergence of commodity index traders affects weekly returns and turn-over during the roll periods. I split the sample (1994–2017) into the pre-financialization (1994–2003) and the post-financialization (2004–2017). I directly test whether the CIT market share (CIT/Open Interest) contributes to commodity returns and whether risk adjustments (based on momentum, basis, basis-momentum, open interest, crowding, and average factors) alter liquidity and insurance premiums documented in Kang, Rouwenhorst, and Tang (2020). I also examine how the financialization affects liquidity and insurance premiums. Finally, since previous results are obtained with Fama-MacBeth regressions, I use an alternative method to test how liquidity and insurance premiums determine commodity returns.