Do economic variables forecast commodity futures volatility?

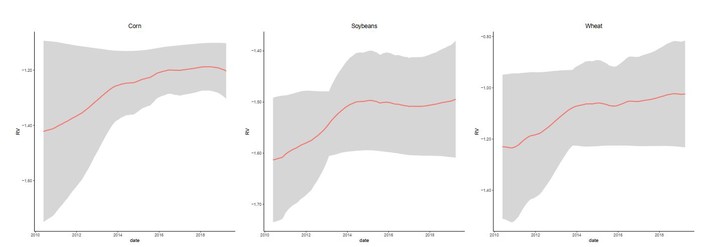

Time varying intercepts

Time varying intercepts

This paper explores empirically whether the supply or the demand uncertainty, the time to maturity, and the slope of the term structure (storage), explain the realized volatility of nearby commodity futures 5-minute returns. I find support for the “uncertainty resolution” and the “theory of storage” hypotheses while the “time to maturity” hypothesis is rejected. These results are robust to the inclusion of autoregressive terms in the baseline model. Next, I evaluate the in- and out-of-sample forecasting ability of models including these economic variables and find mixed results. Finally, I test the validity of these forecasts in expected shortfall modeling.