TechRank (with A. Mezzetti et al.)

Bi-partite graph of companies and technologies

Bi-partite graph of companies and technologies

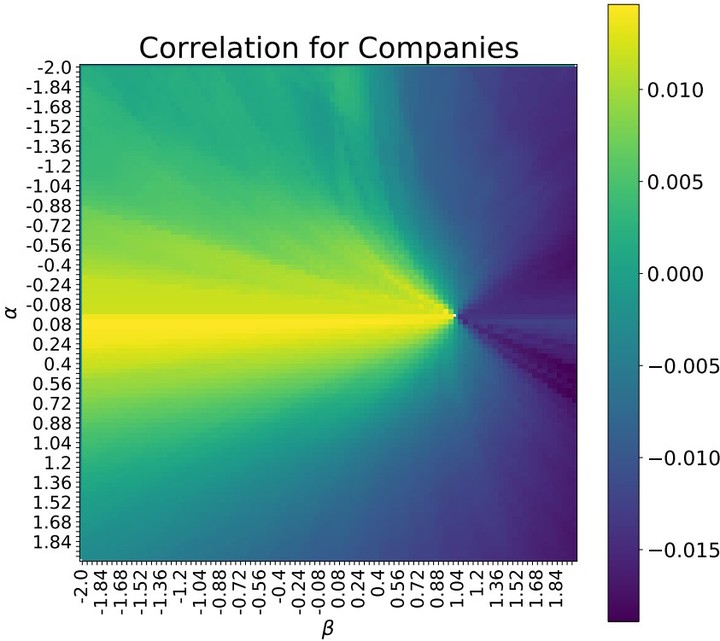

This article introduces TechRank, a recursive algorithm based on a bipartite graph with weighted nodes that the authors developed to link companies and technologies based on the reflection method. They allow the algorithm to incorporate exogenous variables that reflect an investor’s preferences and calibrate the algorithm in the cybersecurity sector. First, their results help estimate each entity’s influence and explain companies’ and technologies’ ranking. Second, the results provide investors with an optimal quantitative ranking of technologies and thus help them design their optimal portfolio. The authors propose this static method as an alternative to traditional portfolio management and, in the case of private equity investments, as a new way to optimize portfolios of assets for which cash flows are not observable.